How E Money Network is the Next Big Thing?

All you need to know about E Money Network Ecosystem

My brother is studying medical science in New Zealand, and every time my parents send him money, they’re burdened with high fees, poor exchange rates, and do not get me started on time it takes. This outdated system not only costs us more but also adds unnecessary stress.

This is not just my problem, many people around the world are facing the same issue.

There should be a better way to make financial support easy and efficient, without the usual headaches.

This is where the E Money Network steps in. With its multi-currency support, low-cost transactions, and MiCA-compliant security, it’s changing the game for cross-border payments. For families like mine, it’s not just about sending money, it’s about making sure support reaches our loved ones quickly, securely, and without breaking the bank. It’s a smarter, more affordable way to stay connected, no matter the distance.

E Money Network goes beyond just simplifying cross-border payments, it’s a complete solution for modern financial needs. In this article, let’s dive into what makes E Money Network so much more than meets the eye.

Introduction

E Money Network is the world’s first public permissioned blockchain with built-in KYC and AML modules. It offers retail users and institutions the ability to tokenize real-world assets using MiCA compliant infrastructure with bank-grade security.

As a Layer 1 blockchain, E Money Network bridges the gap between centralized Web 2.0 systems and decentralized Web 3.0 technologies. Its design focuses on smooth interoperability for DeFi 2.0 and Real-World Asset (RWA) tokenization, allowing better liquidity and accessibility across ecosystems.

E Money Network bridges Web 2.0 and Web 3.0 by providing a secure, compliant, and interoperable infrastructure. It reduces reliance on intermediaries while maintaining the regulatory standards essential for global adoption, making it easier for individuals and institutions to access and trade assets.

Problems Users Face in Blockchain Ecosystems

Lack of Regulatory Clarity

- Users are hesitant to engage with blockchain platforms due to fear of legal repercussions or uncertainty about compliance with regulations.

- Many people steer clear of DeFi platforms because of the lack of basic KYC standards and security concerns. After all, who wants to risk losing their hard-earned money?

High Costs and Slow Transactions

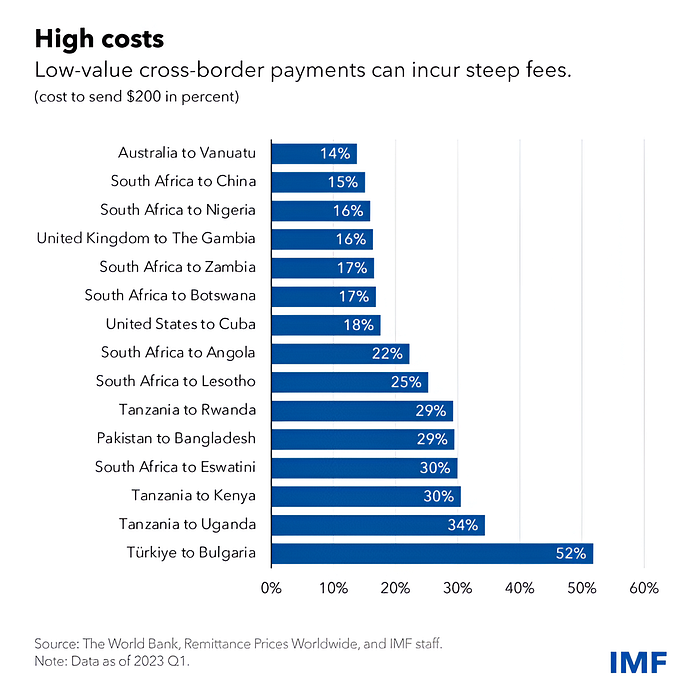

- Traditional cross-border payment systems are slow and expensive. Users need faster, cheaper, and more efficient alternatives.

- According to KarbonCard, banks impose a foreign exchange margin ranging from 1.5% to 2.5%, alongside additional charges. The transaction or SWIFT fee ranges from $50 to $150.

Limited Access to Financial Products

- Users in regulated regions often lack access to blockchain financial products due to non-compliant platforms.

- Many DeFi platforms don’t offer compliant and interest-bearing stablecoins or advanced financial tools that meet users’ needs.

Security Concerns

- Users worry about fraud or using platforms that may inadvertently facilitate illegal activities due to poor compliance.

- A lack of trust in platform legitimacy keeps potential users away.

Fragmented Cross-Chain Ecosystem

- Cross-chain transactions are often complex and risky, making it hard for users to transfer assets across multiple platforms securely and seamlessly.

Exclusion from the Ecosystem

- People without access to traditional financial systems (e.g., the unbanked) or without access to compliant platforms are excluded from blockchain opportunities.

Lack of Device Accessibility

- Blockchain ecosystems have traditionally been designed with desktop computers in mind, which means most platforms and applications are optimized for use on a computer.

- This focus has created a barrier for mobile-first users, especially in developing regions where smartphones are the primary devices for accessing the internet. Since many people in these areas don’t have access to desktop computers, the lack of mobile-friendly blockchain platforms limits their ability to participate in the blockchain ecosystem.

By addressing these challenges, E Money Network enhances user experience, promotes trust, and facilitates participation in blockchain ecosystems effortless and beginner-friendly.

Current Challenges in Crypto Compliance

Lack of seamless KYC/AML

- Compliance is crucial for legitimizing and stabilizing cryptocurrency markets worldwide. Recent violations highlight key compliance areas: Anti-Money Laundering (AML), Know Your Customer (KYC), and adherence to international sanctions.

- KYC and AML are essential regulatory measures designed to prevent illegal activities such as money laundering, terrorist financing, tax evasion, and fraud. These measures are vital in the cryptocurrency industry to ensure transparency, security, and adherence to legal standards.

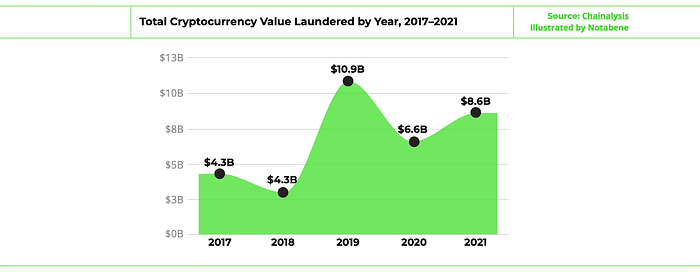

- A 2022 report by Chainalysis revealed that criminals laundered $8.6 billion in cryptocurrency in 2021, marking a 30% increase from the previous year. The report highlights that while billions are transferred from illicit addresses annually, most end up at a small number of services, often designed specifically for money laundering.

Unfortunately, over the years, many cryptocurrency platforms have failed to meet their compliance obligations, leading to significant negative impacts on both their users and the businesses themselves.

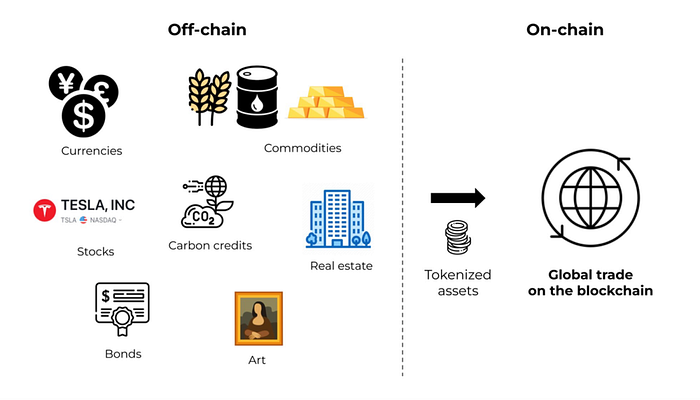

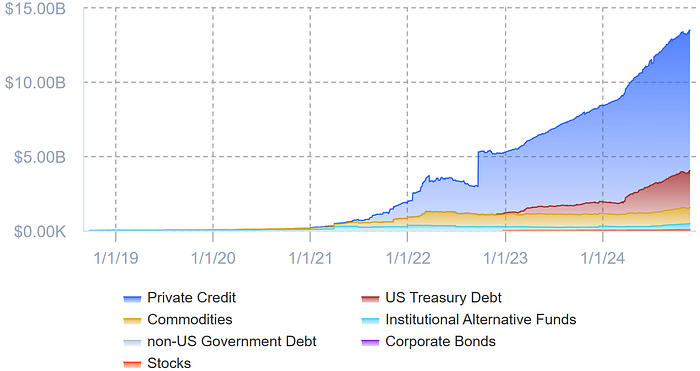

Issues with Tokenizing Real World Assets

- Real-world assets (RWAs) on the blockchain are revolutionizing finance by digitizing ownership of physical and intangible assets. RWAs are Physical or intangible assets represented as blockchain tokens. Tokenization involves converting ownership rights into blockchain tokens, and leveraging distributed ledger technology to track attributes like performance and valuation.

According to The Economic Times, The market value of on-chain real-world assets has surpassed $12 billion, with the potential to reach $16 trillion by 2030.

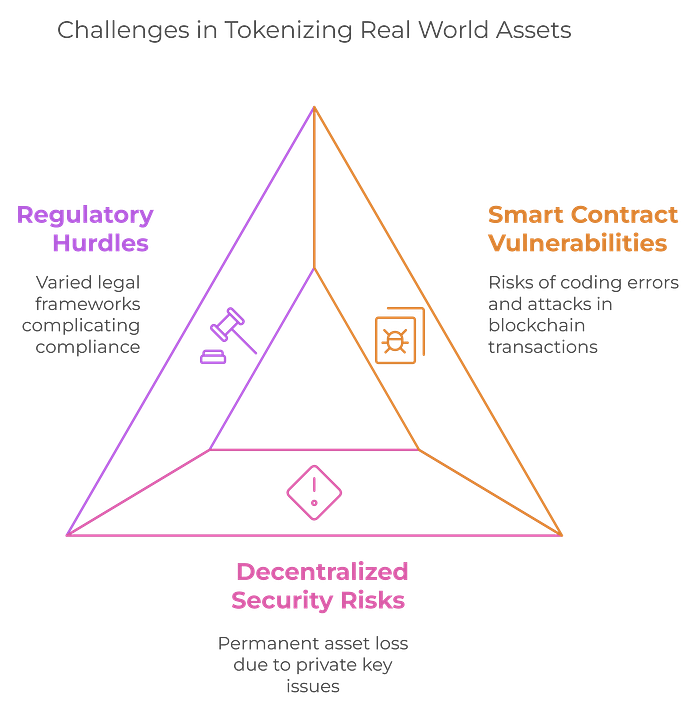

The problem is that the smart contracts, which automate transactions on the blockchain, can be susceptible to coding errors or malicious attacks, potentially leading to investor losses. Moreover, the decentralized nature of blockchain introduces additional security risks, such as the permanent loss of assets if a private key is lost or stolen.

Regulatory hurdles also pose significant challenges for tokenization. The legal framework governing tokenized assets varies widely across jurisdictions, complicating matters for issuers and investors alike. Tokenized assets may fall under securities, property, or tax laws, depending on the jurisdiction, necessitating strict compliance to avoid legal repercussions and maintain investor confidence.

For instance, the U.S. Securities and Exchange Commission (SEC) regulates security token offerings (STOs) to meet traditional securities standards. However, the lack of harmonized global regulations complicates the cross-border trading of tokenized assets.

Let’s check out how E Money Network can handle these challenges by looking at its key features.

Key Features of E Money Network

1. MiCA compliance

The E Money Network is the first MiCA-compliant blockchain globally.

The E Money Network, operating under MiCA regulations, ensures compliance and transparency. With licenses in over 100 jurisdictions, including Canada and Dubai, it adheres to the Payment Services Directive (PSD) and KYC/AML regulations. This makes the E Money Network a trustworthy and secure platform for businesses and investors.

MiCA provides a harmonized regulatory framework across EU member states, allowing licensed crypto-asset service providers to operate cross-border within the EU through “passport” rights. However, it lacks a regime for non-EU providers, making it challenging for global players to interact effectively. The absence of a globally unified framework restricts seamless cross-border trading of tokenized assets.

Suggestions for improvement include collaboration between global regulators (SEC, FCA, MAS, and other key regulators) to develop interoperable standards and frameworks

What is MiCA?

MiCA introduces the term “crypto-asset” as a digital representation of value or rights transferable and storable using distributed ledger technology. Within this framework, e-money tokens (EMTs) represent a specific category of crypto-assets that aim to maintain a stable value by referencing an official currency.

The EU’s MiCA Regulation, adopted on April 20, 2023, provides a regulatory framework for crypto assets across all 27 EU member states, emphasizing stablecoins backed 1:1 by fiat reserves.

MiCA is a proposed regulation that aims to regulate the markets for crypto-assets in the European Union. It covers crypto-assets service providers and a broad range of crypto-assets, including tokens that do not represent traditional fiat currencies.

To give an example, if the company wants to issue a token that represents a commodity, such as gold or silver, it would need to comply with MiCA regulations as an ART issuer.

On the other hand, Tether’s CEO, Paolo Ardoino, has raised concerns about the MiCA framework’s potential risks. He highlighted the regulation’s requirement for stablecoin issuers to hold at least 60% of their reserves in European banks, which could introduce vulnerabilities if banks experience financial instability due to high loan ratios. Despite these concerns, the stablecoins aim to enhance digital payment systems across Europe.

In related news, Norway’s central bank, Norges Bank, has endorsed the MiCA framework, evaluating its potential to support a central bank digital currency (CBDC). While the country is still considering additional regulations to ensure financial stability, it aligns closely with the EU’s MiCA rules, which could shape future developments in cross-border payments and CBDC implementation.

Source of this information, DigWatch.

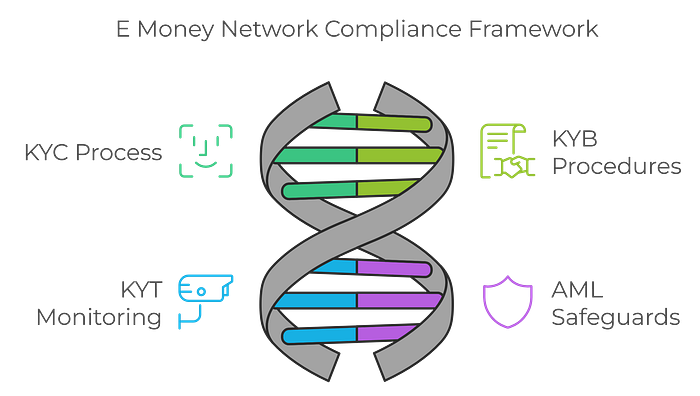

2. KYC, KYB, KYT and AML Modules

E Money Network’s on-chain KYC (Know Your Customer), KYB (Know Your Business), KYT (Know Your Transaction) and AML (Anti-Money Laundering) modules are integral compliance tools designed to ensure security, trust, and regulatory obedience across its blockchain ecosystem.

KYC involves collecting and verifying a customer’s personal information, such as name, address, date of birth, and government-issued identification documents.

KYB is a set of due diligence procedures implemented by businesses to verify the legitimacy and trustworthiness of other businesses they intend to engage with. Similar to KYC, it involves collecting and verifying information about a potential business partner.

While distinct, KYC and KYB work together to create a more secure financial ecosystem. KYC helps to ensure only legitimate customers interact with financial institutions, while KYB verifies that these institutions are partnering with trustworthy businesses.

KYC/KYB screening acts as the first line of defense against financial crime in the crypto space. By thoroughly verifying the identities of both individual customers and business partners, cryptocurrency businesses can identify suspicious activity and prevent criminals from using their platforms for illegal purposes. This not only protects the business itself from potential legal repercussions but also fosters trust and confidence among legitimate users.

These modules address critical compliance needs while fostering institutional adoption and safeguarding against illicit activities.

KYC and KYB Validation

- User and business identities are verified through a centralized entity before participation in the network.

- Only compliant participants gain access, while accounts without verification face restrictions. Transactions from such accounts are automatically rejected by validators.

- This process boosts trust among institutional investors, governments, and enterprises by guaranteeing a secure, compliant ecosystem.

Know Your Transaction

- KYT is a program of monitoring online transaction data to detect and prevent financial crimes such as money laundering and terrorist financing.

- KYT on the blockchain helps to tackle some of the challenges that businesses face with KYC. We’ve seen issues with identification over the decades, from stolen and fake identities to more recent challenges with AI images, video and speech.

- Through real-time scrutiny, KYT identifies anomalous transaction patterns and promptly flags potential risks, safeguarding the system’s integrity.

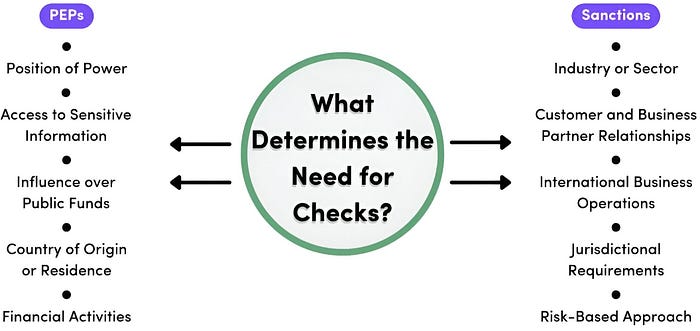

PEPs and Sanctions

- Enhanced due diligence is applied to identify Politically Exposed Persons (PEPs) and screen transactions against global sanctions lists.

- Rapid detection of non-compliant entities ensures adherence to international regulations, strengthening the fight against financial crimes.

Why It Matters?

- Institutions and governments trust the network’s strong compliance measures, opening the way for large-scale adoption of tokenized assets.

- By enforcing identity verification, KYT, and transaction oversight, the platform creates a secure environment for users and businesses.

- Integration of AML modules ensures that the network aligns with global compliance standards, reducing risks of regulatory penalties and reputational damage.

E Money Network’s modular approach delivers a safe and regulatory-friendly blockchain experience.

3. Biometric Bridge

E Money Network integrates biometric authentication, replacing traditional methods like passwords or smart cards.

It's truly amazing that your digital identity is on the blockchain, allowing you to complete the authentication process in the blink of an eye.

It gives protection against fraudulent activities like forging and spoofing. It ensures enhanced security, fraud resistance, and a seamless user experience. This approach leverages blockchain's decentralized, immutable, and auditable nature to provide a highly secure and efficient authentication system.

Imagine accessing your blockchain wallet using just your fingerprint, eliminating the stress of remembering complex passwords or the risk of losing access due to misplaced credentials.

In my opinion, It might be available or able to be used as alternative in case you lost your private key in future.

Why is it important?

Rising Cybercrime and Identity Theft

- 880,418 cybercrime complaints were reported in 2023, reflecting a 10% increase compared to 2022 (FBI Internet Crime Report).

- Total financial losses due to cybercrime reached $12.5 billion in 2023, up from $10.3 billion in 2022.

Data Breach Impact

- In 2023, data compromises in the U.S. hit a record high, marking a 72% increase from the previous peak in 2021.

- 353 million individuals were affected by these data breaches.

FTC Reports on Identity Theft

- In 2023, the FTC received 5.39 million reports; 19% were related to identity theft.

- The most common type of identity theft was credit card fraud, accounting for 40.2% of cases.

Information source, Solulab.

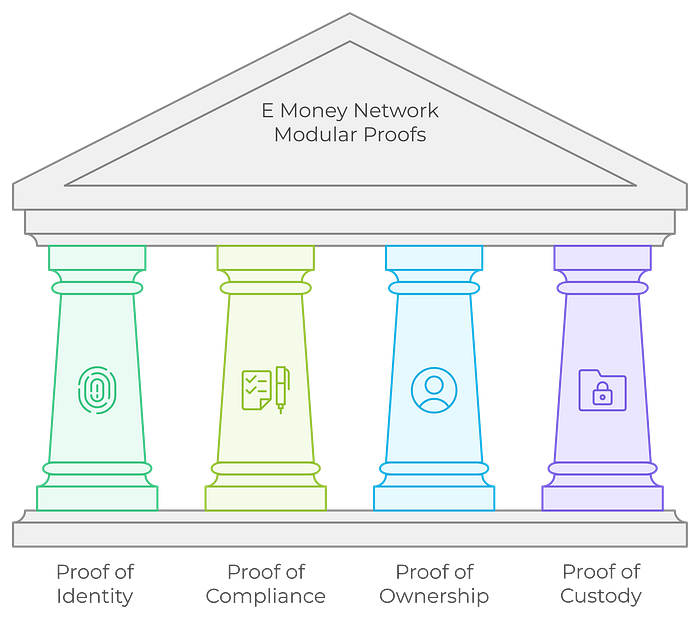

4. Modular Proofs

E Money Network builds a modular foundation with identity, compliance, ownership, and custody proofs

- Proof of Identity

Imagine entering a high-security airport. You pass through identity verification where officials check your passport and ID to confirm you’re an authorized traveler.

On-chain identity verification ensures that all users and businesses are authenticated through digital IDs and KYB processes. This prevents fraudulent entities from entering the network.

2. Proof of Compliance

Before boarding a flight, customs officers inspect your luggage and documents to ensure you’re not carrying prohibited items or violating regulations.

With on-chain KYT and AML modules, E Money monitors transactions to ensure they meet global regulatory standards, keeping the network safe from illicit activities like money laundering.

3. Proof of Ownership

Imagine buying a house. The title deed confirms that you legally own the property. This proof assures everyone that ownership is valid and transparent.

Through on-chain Know Your Ownership (KYO), E Money transparently tracks asset ownership. Zero-Knowledge Proofs are like sealing your title deed in a secure envelope, ownership is verified without revealing personal details.

4. Proof of Custody

A bank vault holds your valuables securely and ensures only authorized access. The vault keeper verifies that assets are safe and managed responsibly.

On-chain custody solutions, including IBAN-linked accounts and Fiat-pegged E-Fiat, act as a secure vault for managing fiat and crypto assets, enabling seamless fiat-to-crypto interaction without any external platform.

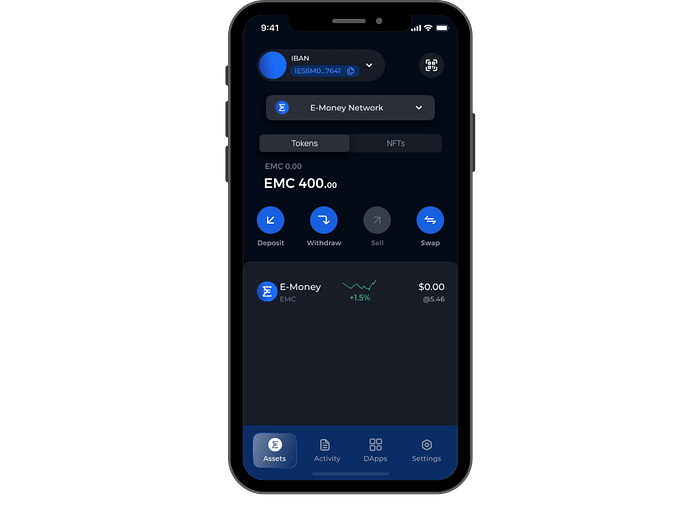

Introduction to E Money Wallet

The E Money Wallet is more than just a tool for managing digital assets — it’s a game-changer in the Web3 ecosystem. As regulatory scrutiny in the crypto space intensifies, the demand for compliant wallets has never been greater. Compliance isn’t just a legal checkbox; it’s the cornerstone of trust, security, and broader adoption of blockchain technology.

The E Money Wallet addresses this need head-on, combining user-friendly design with robust compliance features. By bridging the gap between decentralized blockchain systems and traditional regulatory standards, the wallet creates a secure and compliant gateway for institutions, governments, and individuals to engage in the Web3 space.

Get the wallet from here.

Why E Money Wallet?

Filling the Compliance Gap

As blockchains become integrated into payment systems, financial crime compliance programmes need to adapt.

The compliance gap in the crypto industry is the discrepancy between existing regulatory frameworks and the rapidly evolving nature of cryptocurrencies and digital assets. This gap arises because traditional regulations were not designed to address the unique characteristics and challenges of crypto assets, leading to uncertainty and inconsistencies in compliance requirements.

The E Money Wallet enables secure participation in Web3 without compromising on compliance. Its KYC/AML modules ensure every user meets global regulatory standards, minimizing risks of fraud and illegal activities.

For institutions, this wallet offers a unique opportunity to safely explore crypto transactions while sticking to regulatory framework. By offering these features, E Money Wallet becomes a bridge, it connects traditional finance with the decentralized world.

The Importance of a Compliant Wallet

A compliant wallet isn’t just a convenience, it’s a necessity. Compliance encourages trust, enables smoother onboarding for institutions, and protects users from the risks of non-compliance, such as financial penalties or fraudulent activities.

Key Benefits of E Money Wallet

1. Multi-Chain Functionality

E Money Wallet supports multiple blockchain networks. It allows users to manage, store, and transfer assets from different chains within a single interface.

With this wallet, you can swap tokens between Ethereum and Solana without needing multiple wallets or additional steps.

2. Fiat-Crypto Integration with IBAN Accounts

An IBAN, or international bank account number, is a standard international numbering system developed to identify an overseas bank account.

E Money Network Wallet distinguishes itself with a bank-like registration process. Users undergo secure verification, submitting their ID card, facial features, biometrics, and other relevant information. Upon approval, they receive a wallet address on the E Money Network, which also serves as an IBAN. It combines the familiarity of traditional banking with the innovation of blockchain. This represents a historic milestone as the world’s first Bank on the Chain.

Deposit fiat currency to your wallet’s IBAN account, which is instantly converted into E Money Tokens (e.g., e-EUR) at a 1:1 ratio. These tokens can be used across the blockchain ecosystem.

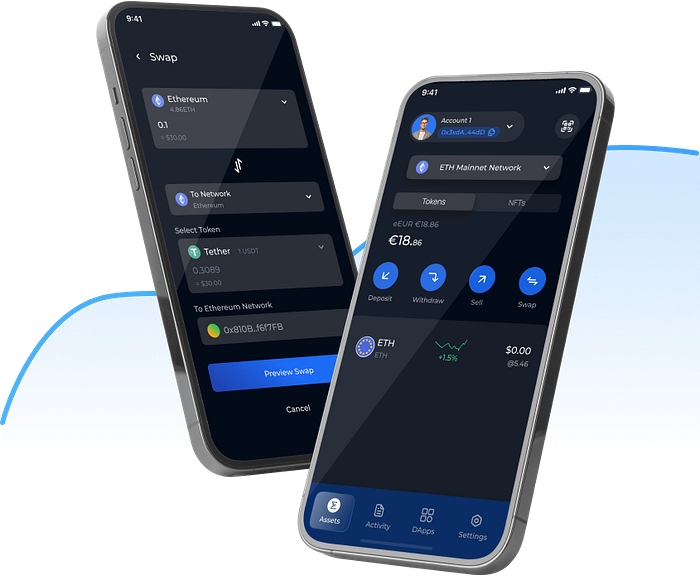

3. Debit Card for Crypto Spending

The E Money Wallet links directly to debit cards, making it easy to spend crypto in everyday life. From buying coffee to booking flights, users can transact easily, just as they would with fiat.

4. Instant Swaps and DEX

The wallet integrates with the E Money Network’s decentralized exchange for quick and cost-effective asset swaps between any digital assets.

You can Instantly convert Bitcoin to e-EUR for international remittances.

5. Support for Foreign Exchange

E Money Wallet simplifies cross-border transactions by supporting over 100 fiat currencies. Users can easily manage international transfers without intermediaries or hidden fees.

In my opinion, With this feature users can take advantage of currency price fluctuations, similar to how traders profit from FOREX trading and users can engage in cryptocurrency trading and potentially make profits from the changing prices of different digital assets.

Here’s a step-by-step video guide on How to create the E Money Wallet.

Read more about E Money Wallet in this blog:

E Money Tokens

E Money Network Wallet uses Scallop’s technology for converting fiat currencies like EUR and GBP into E-Money Tokens.

Scallop is rebranded to E Money Network.

Minting Process

- Fiat sent to the wallet’s IBAN addresses triggers real-time minting of E-Money Tokens.

- E-money tokens are minted and burned on a blockchain based on the monetary value of fiat under custody.

- If a person deposits 100 Euros, 100 E Money Tokens are minted. If they withdraw 50 Euros the next day, 50 tokens are burned, leaving a balance of 50 tokens.

Token Usage

- Tokens can be used within the E Money Network ecosystem.

- Tokens sent to external IBAN addresses are burned, and only the fiat amount is transferred.

Key Features of E Money Token

- Utilizes ZK-Rollups technology for privacy and security by obfuscating transaction details and account balances.

- Enables fast, low-cost global transfers without converting fiat to crypto-stablecoins.

- Sticks to MiCA regulations in the European Economic Area.

- Ensures alignment with fiat and crypto banking standards for user trust and security.

Use Cases in the Solana Ecosystem

1. Plug-and-Play Compliance for Existing dApps

Solana-based dApps like Serum and Raydium can simplify user onboarding and regulatory compliance by integrating E Money Wallet.

Integrating E Money Network ensures users can quickly onboard while complying with KYC and AML regulations. This reduces friction during registration, allowing dApps to focus on delivering core services without compromising on compliance.

This eliminates the need for dApp developers to build custom compliance systems from scratch, significantly cutting down development time and costs.

2. Simplifying Development for New Apps

For developers building on Solana, E Money handles the difficult task of compliance infrastructure.

By removing the complexities of compliance integration, E Money significantly reduces development timelines. Developers can deploy their apps more quickly, capitalizing on market opportunities and gaining a competitive edge.

3. Boosting Solana’s Total Value Locked

The Total Value Locked (TVL) metric is a crucial indicator of a blockchain’s economic activity, reflecting the amount of capital flowing through its ecosystem.

E Money’s compliance features make Solana a more attractive ecosystem for institutional investors and enterprises. By ensuring regulatory alignment and secure transactions, institutions are more likely to deploy significant capital, driving up TVL.

Integrating E Money Wallet into Solana’s DeFi protocols encourages wider participation from both retail and institutional users. The wallet simplifies onboarding and ensures compliance, making it easier for users to contribute liquidity to platforms like Serum, Raydium, and Orca.

Solana’s TVL surpasses $6 billion for the first time since January 2022 with over 40.72 million $SOL locked in DeFi protocols. With E Money Network, Solana’s TVL will boost up.

4. Expanding Solana’s Reach Across Geographies

E Money opens doors to regions with strict regulatory environments, such as Europe. Access to regulated markets can grow Solana’s user base and attract higher-value users. Users in compliant markets tend to have greater purchasing power, increasing revenue growth by big numbers.

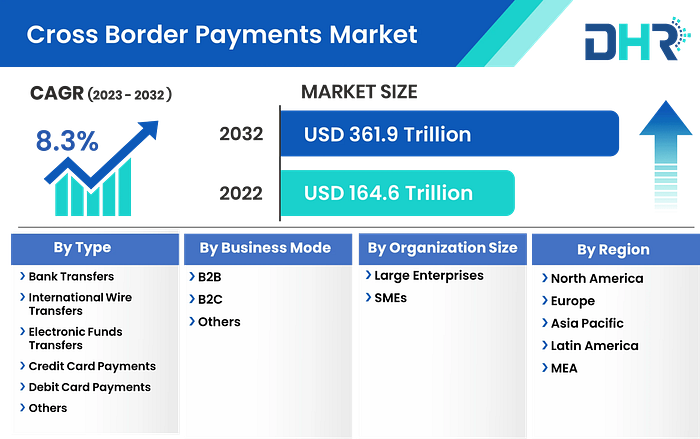

5. Cross-Chain and Cross-Border Compliance

E Money helps in smoother, compliant cross-chain transactions and remittances. Protocols like Wormhole could see a steady rise in asset transfers by leveraging compliant infrastructure.

E Money’s low-cost, multi-currency features provide a competitive edge over traditional remittance systems, tapping into the $165 trillion global cross-border payment market.

7. Mobile Adoption for Mass Market Reach

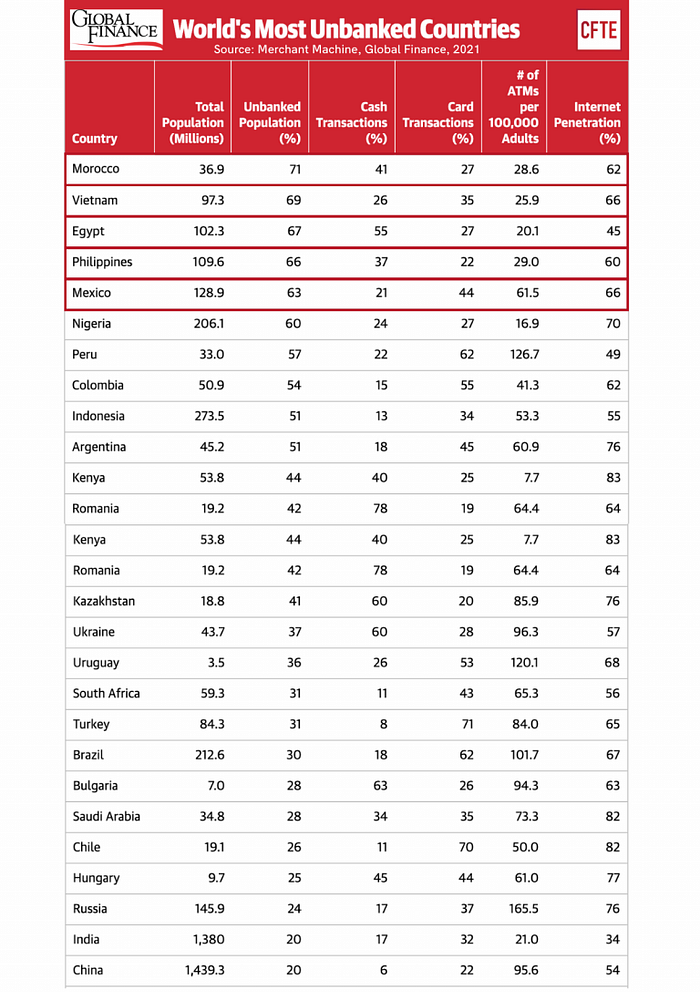

With E Money’s mobile wallet and upcoming IBAN integration, Solana can access a vast, underserved market of 1.7 billion unbanked individuals.

Mobile-first solutions cater to users in developing regions, increasing adoption and driving financial inclusion.

The integration of E Money Network into the Solana ecosystem presents a transformative opportunity to enhance its functionality, user base, and economic impact. By addressing critical areas, E Money enables Solana to grow and innovate more effectively.

Conclusion

E Money Network is a transformative solution for modern financial needs, addressing the pain points of traditional systems in a secure, compliant, and cost-effective way.

By bridging the gap between Web 2.0 and Web 3.0, it provides families, businesses, and institutions with a seamless and efficient way of transferring value globally. This focus on regulatory compliance, user-friendly features such as biometric authentication, and strong support for the tokenizing of real-world assets will push adoption and redefine the future of financial services.

Be it sending money across borders or empowering decentralized finance, E Money Network makes people feel comfortable enough to navigate the blockchain ecosystem.

Thank you so much for reading this far! Your thoughts and feedback would mean the world to me, as it helps justify the effort I’ve put into this.

If you have any queries, feel free to reach out to me on Twitter / X — @GigVivek

To become a part of E Money Network, please join the Discord server:

Explore E Money Network

Citations and Further Reading

Other Sources are mentioned using hyperlinks within the article.